With the 2021 tax filing season just a few months away from starting, the IRS is warning taxpayers to be on the lookout for signs that your identity has been stolen. This month’s newsletter alerts you to some of the common signs of identity theft and what you can do if you discover that you’re an identity theft victim.

Also in this month’s edition, learn about a bank secret that can be yours, tips for dealing with common accounts payable problems in your business, and the story of a Tweet worth $2.9 million!

Please call if you would like to discuss how this information could impact your situation. If you know someone who could benefit from this newsletter, feel free to send it to them.

IRS Warns of Identity Theft Signs

With identity thieves continuing to target the tax community, the IRS is urging you to learn the new signs of identity theft so you can react quickly to limit any damage.

The common signs of ID theft

Here are some of the common signs of identity theft according to the IRS:

- In early 2022, you receive a refund before filing your 2021 tax return.

- You receive a tax transcript you didn’t request from the IRS.

- A notice that someone created an IRS online account without your consent.

- You find out that more than one tax return was filed using your Social Security Number.

- You receive tax documents from an employer you do not know.

Other signs of identity theft include:

- Unexplained withdrawals on bank statements.

- Mysterious credit card charges.

- Your credit report shows accounts you didn’t open.

- You are billed for services you didn’t use or receive calls about phantom debts.

What you can do

If you discover that you’re a victim of identity theft, consider taking the following action:

- Notify creditors and banks. Most credit card companies offer protections to cardholders affected by ID theft. Generally, you can avoid liability for unauthorized charges exceeding $50. But if your ATM or debit card is stolen, report the theft immediately to avoid dire consequences.

- Place a fraud alert on your credit report. To avoid long-lasting impact, contact any one of the three major credit reporting agencies—Equifax, Experian or TransUnion—to request a fraud alert. This covers all three of your credit files.

- Report the theft to the Federal Trade Commission (FTC). Visit identitytheft.gov or call 877-438-4338. The FTC will provide a recovery plan and offer updates if you set up an account on the website.

- Please call if you suspect any tax-related identity theft. If any of the previously mentioned signs of tax-related identity theft have happened to you, please call to schedule an appointment to discuss next steps.

This Bank Secret Can Be Yours

Know the way loans work...and use it to your advantage!

Every banker knows that the majority of the money they make on a loan is made in the first few years of the loan. By understanding this fact, you can greatly reduce the amount you pay when buying your house, paying off your student loan, or buying a car. Here is what you need to know:

Your payment never changes

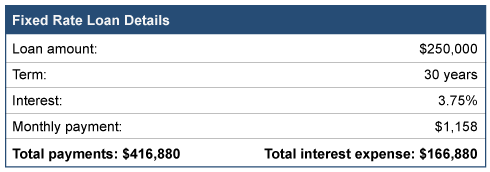

When you obtain a loan, the components of that loan are interest, the number of years to repay the loan, the amount borrowed, and the monthly payment. Assuming a fixed rate note, the payment never changes. Here is an example of a $250,000 loan.

It is important to note that your payment in month one is $1,158 and your monthly payment thirty years later is the same amount...$1,158.

Each payment has two parts

What does change every month is what is inside each payment. Every loan payment has two parts. One is a payment that reduces the amount of money you owe, called principal. The other part of the payment is for the bank, called interest expense. Now look at the component parts of the first payment and then the last payment:

So while your monthly payment never changes, the amount used to reduce the loan each month varies DRAMATICALLY. Remember your total cost of borrowing $250,000 includes more than $166,000 in interest!

Use the knowledge to your advantage

Here’s how you can use this information to your advantage.

For new loans

- Only sign up for loans that allow you to make pre-payments without penalty.

- When borrowing money, keep some of your cash in reserve. Try to reserve a minimum of 10 to 20 percent of the amount borrowed. So in this example, try to reserve $25,000 to $50,000 in cash.

- Immediately after getting the loan, consider using the excess cash as a pre-payment on the note. By doing this you can dramatically reduce the interest expense over the life of the note, all while keeping your payment constant. Even though your monthly payment may be a little higher, the extra payment amount will pay back the loan more quickly.

For existing loans

- Create and look at your loan’s amortization table. This table shows how much of each payment is used to pay down the loan balance and how much goes to your lender as interest. In the above example, 67 percent of the first payment is for the bank, while only ½ of 1 percent of the last payment is for the bank.

- Pay more to you than the bank. Aggressively prepay down any loan until more of each payment goes to you versus the bank. This is the crossover point of your loan.

- Find your sweet spot. After hitting the crossover point, next consider the efficiency of each prepayment and determine when you consider your prepayment ineffective. No one would consider prepaying that last payment when interest expense is only $4.00. But if more than 25% of the payment goes to interest? Keep making prepayments.

Final thought

When you make a prepayment on a loan, reduce the loan balance by your prepayment, then look at the amortization table. See how many payments are eliminated with your prepayment and add up all the interest you save. You will be amazed by the result.

Tips For Dealing With Common Accounts Payable Problems

The accounts payable process is typically very labor-intensive for many small business owners. While moving to a paperless environment may help alleviate some of your accounts payable headaches, there will be new problems you’ll have to successfully navigate.

Here are some of the most encountered accounts payable problems and several solutions to consider.

Common problems with accounts payable

- Double payment. A vendor sends you an invoice for $100. Your company promptly pays this vendor $100, but a short time later another payment for $100 goes out to the vendor. Sometimes this can be the fault of the vendor sending an invoice in different ways (i.e. via fax and e-mail). Or the vendor moves to digital invoicing and emails more than one person in your company, effectively duplicating the invoice electronically. Or even worse, you print out a digital invoice twice.

- Vanishing invoices. Your company could get an invoice from a vendor and have that invoice get misplaced, or the invoice accidentally gets destroyed before ever making it into your A/P system. With digital invoices, how do you know which one is the original and which one is a duplicate?

- Sending payment prior to delivery. There are sometimes benefits to paying an invoice as soon as possible. However, if your company pays an invoice before a shipment arrives, that could lead to an awkward conversation with your vendor if any of the shipment arrives with damaged or missing items.

- Matching errors. A manual investigation is often required if a discrepancy is discovered between purchase orders, invoices and other documents. This often happens when multiple invoices are paid with one check, and the breakout of the invoices does not fit on the check stub or other payment documentation. It gets more complicated if your supplier applies payments haphazardly creating a past due account, all while you continue to pay the bills.

What you can do

- Update your internal controls. Have your A/P team help update internal processes and document how invoices should be handled. Pay special attention to separation of duties and full use of purchase orders to ensure invoices are accurate.

- Have one inbox for A/P. All e-mails with invoices should go to one inbox. This will help reduce the chances that an invoice will be received or paid twice. Limit access to this billing address.

- Limit access to cash accounts. It’s more important than ever for someone without authorization to your company’s cash accounts to review bank reconciliations. Not only will this help to potentially uncover erroneous payments, but it could also help to uncover potential fraud that is occurring in your company.

- Track key performance indicators. Create a report each month of all unpaid invoices and another report that shows payments made. Explore bank security features to identify duplicate payments and allows you to control checks that are confirmed for payment. Use your accounting software to help identify duplicate dollar amounts and duplicate invoice numbers.

- Be cautious with ACH. Giving a vendor automatic access to your firm's checking account needs to be tightly controlled. Explore ways to ensure you are reviewing these auto payments on a timely basis and that you are receiving supporting invoicing of these payments.

Please call if you have any questions about improving your business’s accounts payable process.

The Tweet Worth $2.9 Million!

The collectibles industry used to be defined by classic keepsakes such as stamps, coins, and trading cards. Today, a new kind of collectible called non-fungible tokens (NFTs) has exploded in popularity. From music to digital game pieces, NFTs are digital assets that sometimes sell for millions of dollars. Twitter co-founder Jack Dorsey sold his first-ever Tweet as an NFT for $2.9 million!

But is there any substance behind the hype? And what does it mean for you?

Understanding NFTs

NFTs offer a blockchain-created certificate of authenticity for any digital asset. This asset can be a piece of music, a token for a popular game, or a piece of digital art. To understand an NFT, consider its components:

Non-Fungible...Where cryptocurrency like a Bitcoin is designed to be readily tradable (fungible), non-fungible is just the opposite. There is one and only one of it.

Token...In this case the non-fungible identification is attached to a specific digital asset or token.

Therefore, each NFT is unique and can readily solve the problem of users creating multiple copies of a digital asset. In effect, Jack Dorsey's original tweet cannot be copied or duplicated because of NFT technology!

Why NFTs are popular

Traditional artists rely on auction houses and galleries to sell their work. These galleries and auction houses authenticate the work as original. Now artists can sell digital works at the same prices as rare works of art by using NFTs to do the authentication work for them. It is so popular now that even companies are getting in on the action. For example, a Charmin digital brand was auctioned off to raise funds for charity.

Why some NFTs are so expensive

Just like physical collectibles, there’s a market for NFTs. Current NFT buyers tend to be tech workers and entrepreneurs who understand the intricacies of purchasing digital goods. Artists are also dipping their toe into the NFT waters. For instance, superstar artists like King of Leon and Steve Aoki have sold NFTs for millions of dollars. Just imagine if your favorite musician decided to record an exclusive piece of music and then only sell 100 copies of the song. How much would you pay?

What you need to know

Here’s what you need to know about getting involved with NFTs:

- Large cash outlay not necessary to invest. There are multiple NFT marketplaces where you can get involved as a buyer without getting into 5- and 6-figure bidding battles. Some of the more popular marketplaces are Opensea, Rarible, SuperRare and Nifty Gateway.

- Beware of fees to create NFTs. If you want to create your own NFT, you’ll likely spend hundreds of dollars in various fees to make your own tokens. If you end up selling your tokens, you may be able to cover the cost of these initial fees. If you struggle to sell your tokens, however, you’ll end up eating the cost of creating the tokens.

- Do your research. Since NFTs are so new, there isn’t a lot of history to judge its performance. As with any investment, you could either make a fortune, lose everything you invested, or end up somewhere in between. And these digital assets are treated just like other property, so you would pay capital gains taxes if you sold an NFT at a profit.

- NFTs require power. NFTs use blockchain technology. Blockchain technology requires power. Lots of it. There is growing concern on the energy usage for this new digital marketplace and whether it is sustainable.

Because NFTs are becoming so popular, so fast, many experts are leery of what the world of NFTs will look like in the future. Regulation is currently lacking, and legal precedence is unclear. While blockchain technology can verify your purchase, does owning the NFT of something really mean you own the asset? Will NFTs stand up in court? These are some of the questions being asked without concrete answers.

As always, should you have any questions or concerns regarding your tax situation please feel free to call.